Have you heard of ‘HGTV Syndrome’? That’s a reference to the impact that home renovation shows had on new homeowners over the last decade. Stainless Steel appliances, open living spaces, and granite countertops have become expected standards for recent first-time homebuyers. We get it. Quality home spaces are more important than ever, but remember they come at a cost…a cost that should be carefully considered if you want to prioritize your financial wellness.

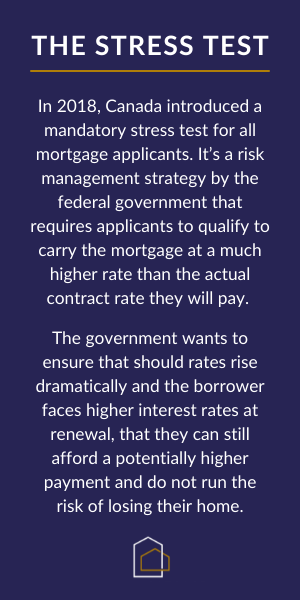

Mortgage approval tools – like the Stress Test – exist to help Canadians avoid over-borrowing. However, there are more considerations at play than how much you qualify for. The scary truth is that financial institutions can give more than enough credit for you to get in trouble with. This applies to individuals at all income levels. In the end, we are responsible for our own personal financial health and a proactive approach is required to avoid future financial difficulty.

In April 2020, Susanna Penning was invited to join CHRI’s radio show, Let’s Talk Money and discuss the concept of responsible borrowing as it relates to Canadian Mortgages. The wisdom shared in that conversation has been summarized below into five important tips that can apply to all Canadians and their credit habits regardless of salary.

#1 – Don’t Spend What you Qualify For

It’s tempting to use what you qualify for as your home shopping budget. But wait! Your mortgage approval budget should be considered a yellow light, not a green one. Our advice is to make note of that top figure, but proceed with caution.

Remember that what you qualify for is just a snapshot in time. It’s the maximum value of home financing available to you on the date you were approved. That number doesn’t show what you spend on your lifestyle post mortgage payment, see #2 below. It also doesn’t show the stress you will feel if you find your income compromised for unexpected reasons, see #3 further below. If you spend what you qualify for now then you aren’t preparing yourself for the future.

Our advice when it comes to responsible borrowing is to consider the benefit of a manageable payment structure over the biggest home you can afford. Financial freedom is a huge win in everyday living that should not be underestimated.

#2 – Manage Discretionary Spending Habits, Try Saving

Discretionary spending adds up quickly and doesn’t show up in the typical mortgage approval process. Lifestyle costs like lattes, events, and travel vary significantly between individuals and can pose a real threat to financial wellness. Everyday spending habits deserve serious consideration and only you can make that an ongoing priority.

Our advice when it comes to responsible borrowing is for mortgage applicants to “test drive” how much they can save leading up to their home purchase. A strong financial plan should always include cash reserves to weather storms ahead and your mortgage payment should be structured to allow you to continue to save money as well.

$28 dollars per day adds up to $10k per year.

your spending habits matter

#3 – Plan for Compromised Income

The future is full of unknowns! Your mortgage was approved, based on your income source at that time. Is that income always going to be stable? When it comes to responsible borrowing, ask yourself: What payment can I afford on a monthly basis if my income is compromised?

Loss of job, maternity leave, and potential disability are all serious considerations for your future income. A typical mortgage term is 5 years…and a lot of changes can happen in that time. We’ve seen a number of applicants who don’t expect to become parents before they renew their mortgage but then, well…life happens!

For a couple that is looking to purchase a home, we recommend structuring mortgage payments on one income. Does this reduce the home shopping budget? Absolutely. But it can also lead to more savings and lump sum mortgage payments that allow you to pay that debt down as quickly as possible. Even better, it creates the opportunity for you to welcome unexpected changes in life without added financial stress. That’s a HUGE benefit that comes with responsible borrowing.

#4 – Use Credit for Emergencies, Mostly

Credit cards and lines of credit aren’t bank accounts. They offer convenience and security in case of emergencies. When it comes to credit, responsible borrowing means using those products for the convenience they offer but being diligent in paying that debt off every month. If you have to carry over a small balance, endeavour to pay it off the next month. Carrying credit balances month-to-month is a signal that you may not be borrowing responsibly.

A common financial pitfall for first-time homebuyers is using their credit to finance house upgrades and big lifestyle purchases post move-in. Don’t forget! Whatever you put into your house after you buy it is also part of responsible borrowing. If those purchases didn’t exist when home financing was approved, they were not considered in that “snapshot.” Debt financing these purchases can lead to liability trouble down the road. Impulse buying is a real threat to responsible borrowing and we all need to manage the greed in our own hearts.

#5 – Don’t Use your Home as a Bank Account

Beware of perpetual refinancing your home. Draining the equity from your home every five years to pay off credit card debt and buy new “toys” only increases your mortgage without ever paying it down.

Your home should be one of the bigger assets in your financial portfolio, if not the biggest. Part of responsible borrowing is planning to accumulate wealth by gaining equity in your home.

Remember: It’s Okay to be Conservative about Finances

We sympathize with homebuyers in today’s real estate market. It’s more difficult than ever for people to afford homes. In addition to that, the socially accepted standard of a first home continues to rise. While many first time buyers are turning to the bank of mom and dad, not everyone has access to that kind of support.

If you are house shopping, we’re here to remind you to keep your own HGTV syndrome in check. Don’t forget that it’s ok to be conservative when it comes to finances and do endeavour to be accountable for your personal spending habits.

Our hope is everyone lines up with a professional and gets good advice. Mortgage brokers have a lot of wisdom and experience when it comes to financial wellness and they add a lot of value to the buying process. The best ones care about you and have your best interest at hand. If you are looking for strong mortgage advice, reach out to our team. We want to see your homeownership dreams succeed!

Trackbacks/Pingbacks